Accounting transaction ledger

A wide variety of screens and reports are available to view general ledger history. The data flow is as follows: Account numbers are assigned during software installation from your chart of accounts to every RDP transaction code. Transaction codes are posted within the RDP system to reservations, folios, groups, companies, travel agents, wholesalers, etc. The balanced daily journal entry is exported to a network transfer file. The daily totals are transferred to your back-office system, but the detail behind the total is in RDP.

The detail of each of the calls is in the RDP system in the transaction detail report. General Ledger history is stored forever in the RDP system and limited only by available disk space. Advance deposit ledger, guest ledger, and city ledger reports are available from RDP.

Monthly income statements, balance sheets, cash flow reports, etc. As part of the night audit process the RDP system tracks the following ledgers: Guest Ledger The sum on the balance due of all guests currently checked-in. City Ledger The balance due from all groups, companies, and wholesalers. Travel Agent Ledger Tracks all payables and prints checks to travel agents. Owner Ledger Includes a complete condominium and timeshare owner accounting ledger.

Credit Card All credit card payments are tracked and reconciled. These values are then passed through the accounting system resulting in an adjusted trial balance.

This process continues until the accountant is satisfied. Financial statements are drawn from the trial balance which may include:.

For the purposes of accounting, please forget what you know about credits and debits. In accounting, debit Dr. An account will have either a " normal credit balance " or a " normal debit balance ", depending on the type of account. The normal balance indicates which side of the account the amount goes to when the account balance increases. For example, the account 'Cash' has a normal debit balance: Debits and credits may be derived from the fundamental accounting equation.

They result from the nature of double entry bookkeeping. Two entries are made in each balanced transaction, a debit and a credit. This allows the accounts to be balanced to check for entry or transaction recording errors. In accounting this is generally rewritten from the perspective of the business or commercial entity the books detail:. Entries in the books are in pairs and track the advantage or asset of the company simultaneously with the disadvantage or liability.

In this view the Owner's equity is a claim of the investor against the company. Even when a business has a single owner we make a distinction between the owner's assets and the assets of the business. For example if the owner gives a van to the business this will count as capital introduced, if the owner takes a salary this will be accounted for as drawings.

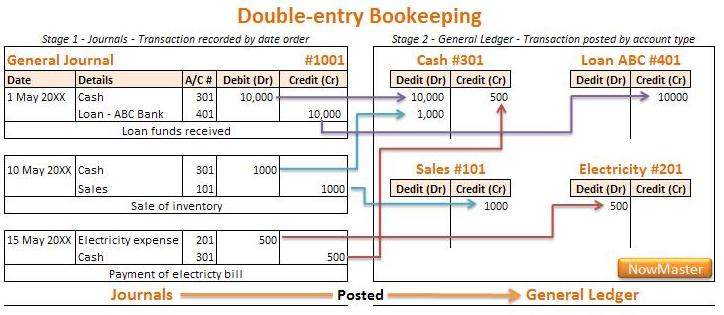

All accounting transactions are first recorded in a journal. The most common of these is the General Journal , sometimes also known as the Book of Original Entry, because it is the first place a transaction is entered into the books. Journal Entries are made from source documents , which can be anything from receipts to invoices to bank statements. These two entries show the premise of double-entry accounting.

Note that the form of what is written is as important as the actual text:. One representation of an account is called the T-account , shown above. A T-account contains just the basic elements of the account, so it lacks the necessary detail for use in bookkeeping operations.

However, it has its uses as both an illustrative tool and a quick reference. Each account needs to have a unique Account Name , such as Cash, for ease of reference later on.

In modern accounting systems, you will often see an account number alongside the name in order to facilitate report generation and computer entry. Under the bar are the debit from the Latin debere , to owe and credit credere , to believe columns. As it shows in the example above, the balance of a T-account can be figured by first totaling each column. Second, subtract the smaller subtotal from the larger, and finally placing the total in the larger number's column.

While a T-Account is useful for quickly summarising an account's balance, it only contains a fraction of the information that was recorded in the Journal. A central axiom for accounting is the accounting equation above. Depending on the type of company involved, Owner's Equity may be "Shareholder's" or simply "Equity", but the equation holds.

The list of all of the accounts along with their respective account numbers is called the Chart of Accounts. Asset accounts indicate what a company owns. This can be actual possession or the right to take possession, such as a loan extended to another company.

Some assets are identifiable by the term "Receivable". Assets have a normal debit balance. Liability accounts indicate what a company owes to others.

Examples of liabilities include loans to be repayed and services that have been paid for that the company hasn't performed yet. Many liabilities can be identified by the term "Payable" in their account name. Liabilities have a normal credit balance. Equity accounts are a group of accounts that represent the amount of owner's equity in the business. There are four main types of Equity accounts:. Assets and liabilities should be recorded at the price at which they were acquired.

This is to ensure a reliable price; market values can fluctuate and be different between differing opinions, so the price of acquisition is used. Expenses should be matched with revenues. The expense is recorded in the time period it is incurred, which means the time period that the expense is used to generate revenue. This means that you can pay for an expense months before it is actually recorded, as the expense is matched to the period the revenue is made. Revenues should not be recorded until the earnings process is almost complete and there is little uncertainty as to whether or not collection of payment will occur.

This means that revenue is recorded when it is earned, which means the job is complete. The Income statement is a list of all inflows and outflows of economic benefits revenues and expenses. It follows the general subdivision of business activity into trying to make money by operating activities, investing activities, and financing activities.

Operating activities include the main business that is concentrated on, and paying taxes on this business, as well as interest for liabilities from owning non-current assets such as machinery to run the business. Investing activities include cash used for investment in plant and equipment or recovered from sale of plant or equipment, and money made outside of the main business activity using resources available from the business: Financial activities are cash activities undertaken when other entities invest in the operations of the main business.

So finance activities include cash from issuing shares in the company, cash given as dividends to shareholders, cash from borrowing and cash out due to borrowing repayment. A few items are reported as netted if they are sufficiently short term or liquid such as other investments, equity shareholding changes: Net cash increase decrease in cash held