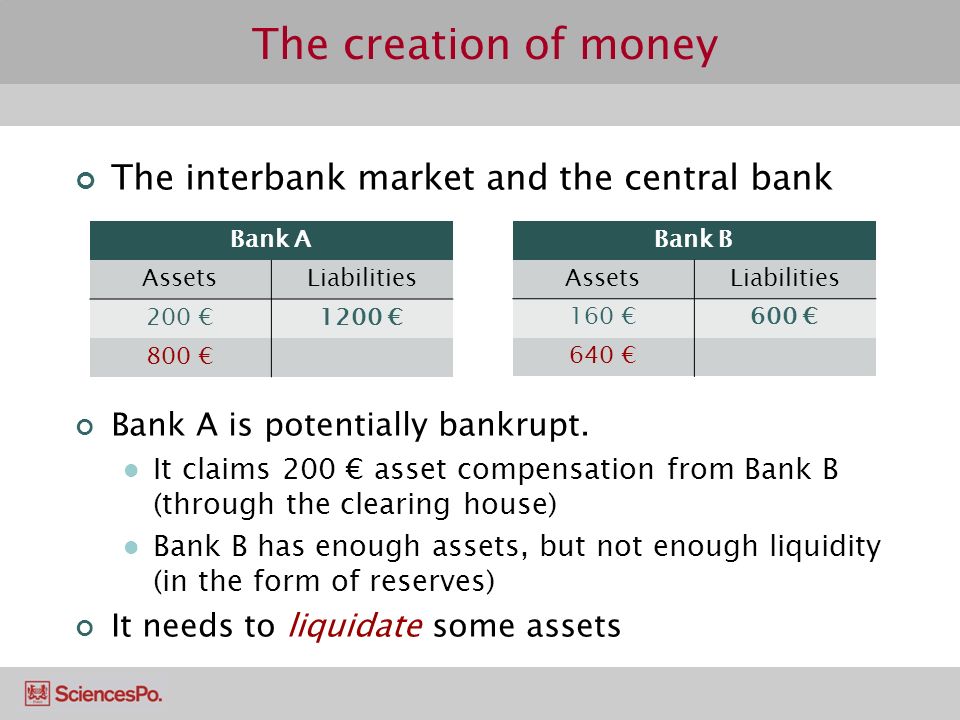

Interbank market liquidity and central bank intervention and money

This provides further evidence that the interbank market was not completely frozen through the crisis. However, it seems likely that unmet demand existed in the market.

Banks that would be expected to demand more funds, such as banks with higher pre-crisis reliance on repo funding, did not increase borrowing in the fed funds market. We see sharp differences between large and small banks in their access to credit: Large banks show reduced amounts of daily borrowing after Lehman and borrow from fewer counterparties. Assuming that in the very short run banks do not change their demand for liquidity, these results are consistent with credit rationing of large banks.

In contrast to some theoretical models, we do not find evidence of a complete cessation of lending, nor do we find evidence that riskier lenders are more likely to hoard liquidity at the height of the crisis. The views presented are those of the authors and do not necessarily represent the views of the Federal Reserve Bank of New York or the Federal Reserve System. Financial markets Global crisis. What happened to US interbank lending in the financial crisis?

Many academics have documented the impact of the recent crisis on interbank funding, with mixed results: UK — Precautionary hoarding by settlement banks Acharya and Merrouche , fewer interbank lending relationships during the crisis Wetherilt et al. General stability in the aggregate fed funds market The overnight federal funds market was remarkably stable through the recent period of turmoil in the financial markets.

Figure 1 shows daily amount of transactions and daily interest rate in the fed funds market, highlighting four key dates: The daily amount of transactions was surprisingly stable through the period, and began to fall only after the interest on reserves IOR period begins.

The weighted average rate then jumped, with substantially more widening of the distribution. Tougher times for riskier banks The relative stability of amounts borrowed masks a dramatic shift in the flow of funds and the distribution of rates across different borrowers.

Worse performing banks do not lend less We do not see the same patterns in lending as we do in borrowing. Banks not indiscriminately driven to the discount window, but unmet demand likely While we appear to document a functioning fed funds market immediately after the Lehman crisis, we only measure loans that were made, not all the loans that banks might have wanted.

The EMU after the euro crisis: Insights from a new eBook. Brexit and the way forward. Deepening EMU requires a coherent and well-sequenced package. Spring Meeting of Young Economists Economic Forecasting with Large Datasets. Homeownership of immigrants in France: Evidence from Real Estate. Giglio, Maggiori, Stroebel, Weber.

The Permanent Effects of Fiscal Consolidations. Demographics and the Secular Stagnation Hypothesis in Europe. Independent report on the Greek official debt. Step 1 — Agreeing a Crisis narrative.

A world without the WTO: Lending facilities include loans for maintaining daily liquidity, collateralised by eligible securities. Deposit facilities include excess liquidity deposits with the National Bank of Serbia.

Interest rates on standing facilities constitute the ceiling and floor of the corridor of interest rates in the interbank market. As an important control factor in managing banking sector liquidity, they ease the fluctuations of short-term interest rates in the interbank market which would be more pronounced without such facilities. Interest rates on standing overnight facilities, i. In inflation targeting regime, foreign exchange interventions are an infrequently used secondary instrument which contributes to the achievement of the targeted inflation rate after the effective impact of the key policy rate has been exhausted.

In addition to applying the above main monetary policy instruments, the National Bank of Serbia also approves to banks short-term liquidity loans against collateral of securities.

In and , these loans were approved in support of financial stability, whereas since 1 January , they are approved to facilitate liquidity management for banks. They are extended at auctions and have the maturity of up to one year. Monetary Policy Monetary Policy Instruments. Monetary Policy Instruments The main monetary policy instrument of the National Bank of Serbia is the key policy rate — interest rate applied in its main open market operations currently, reverse repo transactions — repo sale of securities, with one-week transaction maturity.

Open Market Operations The National Bank of Serbia conducts open market operations in order to regulate banking sector liquidity, influence short-term interest rate movements and signal its monetary policy stance. Principal Characteristics of the Open Market Operations Concept Required Reserves Required reserves are the amount of funds that banks are required to keep on deposit in accounts with the central bank.