Latest bitcoin block mined

Because each block contains a reference to the prior block, the collection of all blocks in existence can be said to form a chain. However, it's possible for the chain to have temporary splits - for example, if two miners arrive at two different valid solutions for the same block at the same time, unbeknownst to one another.

The peer-to-peer network is designed to resolve these splits within a short period of time, so that only one branch of the chain survives. The client accepts the 'longest' chain of blocks as valid.

The 'length' of the entire block chain refers to the chain with the most combined difficulty, not the one with the most blocks. This prevents someone from forking the chain and creating a large number of low-difficulty blocks, and having it accepted by the network as 'longest'. There is no maximum number, blocks just keep getting added to the end of the chain at an average rate of one every 10 minutes. The blocks are for proving that transactions existed at a particular time.

Transactions will still occur once all the coins have been generated, so blocks will still be created as long as people are trading Bitcoins. No one can say exactly. There is a generation calculator that will tell you how long it might take.

You don't make progress towards solving it. After working on it for 24 hours, your chances of solving it are equal to what your chances were at the start or at any moment. Believing otherwise is what's known as the Gambler's fallacy [1]. It's like trying to flip 53 coins at once and have them all come up heads. Each time you try, your chances of success are the same. There is more technical detail on the block hashing algorithm page.

Retrieved from " https: Navigation menu Personal tools Create account Log in. Views Read View source View history. Sister projects Essays Source. When sending Bitcoin, a fee needs to be paid by users - called a transaction fees. This exists to incentivise miners to include transactions in mined blocks.

It's effectively a bidding war to get your transaction into a block, where whoever pays the highest fee is processed first. A side effect of high demand for sending Bitcoin is more transactions being sent, and higher fees. This transaction fee is given to miners, so essentially - the more congested the Bitcoin network, the more money miners earn.

This fee is essentially an extra payment sent with any Bitcoin transaction, and can be worked out by subtracting the outputs from the inputs of a transaction. As the block reward coinbase reduces over time, if Bitcoin price doesn't increase at the same rate - these fees can provide an incentive for miners to continue mining. So when you start mining, you might have a dream of getting say BTC in a week. You need to be aware that there is a huge number of people competing to create new blocks.

By creating a new mining pool by yourself, the chance of getting this block reward is extremely low - although if you did get it by chance, you'd get a significant reward.

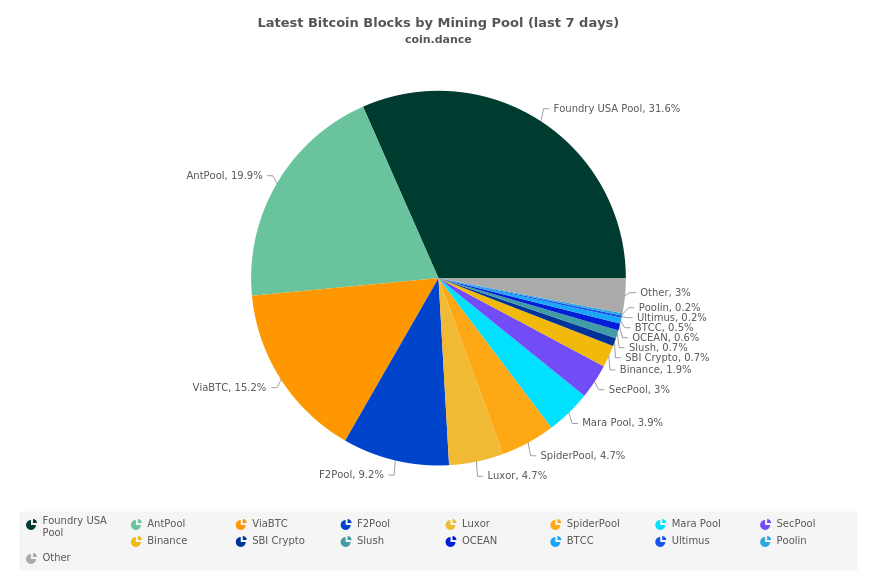

Instead, most miners join an existing mining pool - where they'd get a more steady income rather than having to wait years for a block reward to themself. Mining pools are large groups of miners, where if any one of them creates a new block - the reward is shared based on how much work each miner contributed.

Work is defined in hash power or hashrate, which in general means how many guesses can be made per second for the required hash. The split between miners differs between mining pools, we're going to use Slushpool as an example in this guide - but you can see how other pools work here.

Slushpool, which has For example if the goal is a hash that consists of 18 zeros, a miner can submit any time after they've found the first 8 - which would prove that they've done work to get this far. They'd need to get all 18 zeros to win the block, but it would at least prove the miner is putting the effort in - and so they should be rewarded for it.

The split is counted by the amount of work they have proved vs the total work proven by all the miners in the pool. Lets step back a moment though, now that we know how much work everyone's done - how is the reward distributed?

The block reward for the miner who was lucky enough to find it would be very large, a lot more than the miner will see as a return from the pool in the short term. What stops the miner taking that reward and leaving as if they were in their own pool? Well the blocks are pre-built by the pool. Everything except the nonce the value in the block that miners change to get a hash with a certain amount of preceding zeros must stay the same.

One would assume that the pool can then just verify the nonce, and rewards wouldn't be awarded if the user changes the address as the hash won't pass when being verified by the pool - incentivising miners to follow the pool's rules although we are yet to find documentation on this.

This part is nice and simple. Whichever pool guesses a Block's hash first wins the Block reward. The more hashing power a pool has, the higher the probability that the pool will succeed. Extend this over a long period of time, then the reward split between pools should be similar to the share each pool has of total hashpower. Slushpool for example, which currently has This site cannot substitute for professional investment or financial advice, or independent factual verification.

This guide is provided for general informational purposes only. The group of individuals writing these guides are cryptocurrency enthusiasts and investors, not financial advisors. Trading or mining any form of cryptocurrency is very high risk, so never invest money you can't afford to lose - you should be prepared to sustain a total loss of all invested money.