Kraken exchange review 2017

27 comments

Bitcoin miner open source code

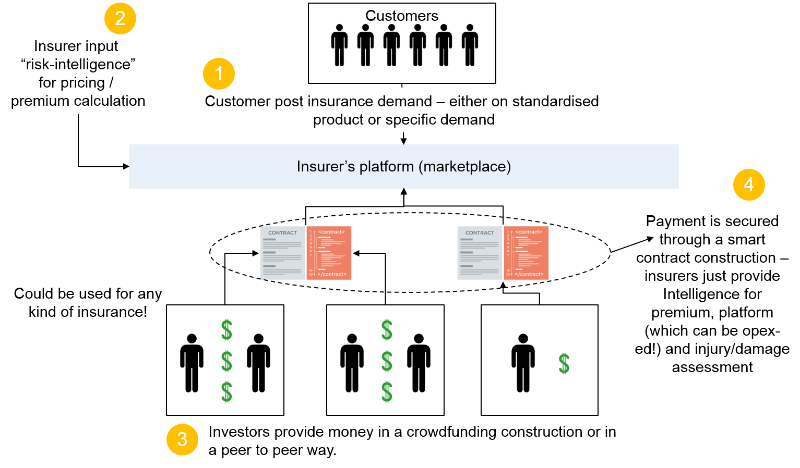

Peer-to-peer insurance is a reciprocity insurance contract through the Collaborative consumption concept. The aims of peer-to-peer insurance are to save money through reduced overhead costs, increase transparency, reduce inefficiencies, [1] and especially to reduce the inherent conflict between insurance carriers and their policyholders at the time of a claim.

There are many types of peer-to-peer insurance. The first type was created by Insurance broker as opposed to insurance companies. In this broker model, insurance policyholders will form small groups online. A part of the insurance premiums paid flow into a group fund, the other part to a third party insurance company.

Minor damages to the insured policyholder are firstly paid out of this group fund. For claims above the deductible limit the regular insurer is called upon. If the group pool happens to be empty, a special insurance comes into force. More recently, models created by insurance companies have arisen.

The insurance model is similar to the broker model except that as the peer-to-peer provider is the actual insurance company. If the pool is insufficient to pay for the claims of its members, the insurance carrier pays the excess from its retained premiums and reinsurance.

Conversely, if the pool is "profitable" i. Peer-to-Peer insurers take a flat fee for running the operations of the insurance enterprise. The fee is not dependent upon how many or how few paid claims there are. A group can be set up by the policyholders, forming a social network somewhat like Facebook. In the broker model, the only requirement is that all group members must have the same type of insurance.

Examples are liability insurance , household contents insurance , legal expenses insurance and electronics insurance. In the carrier model, the only requirement is that the group members have something in common, such as being members of the same club or believing in the same charity. In the broker model, the peer-to-peer insurance concept carries no costs other than the special insurance.

The providers are financed through brokerage commissions of insurance companies. In the carrier model, the peer-to-peer insurance concept carries no cost other the fixed fee to the carrier's management and the cost of reinsurance and other more minor expenses.

One of the earliest peer-to-peer insurance brokerage models was developed by the German Alecto GmbH, Berlin. In , this brokerage version peer-to-peer-insurance-model was first introduced in the German insurance market under the brand Friendsurance. The peer-to-peer approach aims to strengthen the sense of responsibility towards the group while minimizing the number of fraudulent cases. In , about 90 percent of those who took advantage of the peer-to-peer-insurance model were repaid contributions.

In , the British insurance company Guevara introduced the peer-to-peer insurance concept for car insurance in the UK. Also in , P2P Protect Co. The platform was launched operationally in November with a product range referred to on the platform including Marriage Safety, Child Safety and Family Unity. In , [[ Huddle Insurance ]] launched [18] in Australia, initially with a peer-to-peer model of insurance, with plans to expand into peer-to-peer lending in the future.

Besure, a Canadian company from Calgary, and Otherwise in France has also announced their launch for Darwinsurance in Italy is listed [21] as the first Italian company who launched peer to peer insurance model in Participants in peer-to-peer insurance are given more control over their coverages. Control ranges from allowing peers to form their own risk pools for deductible coverages [23] to allowing peers to make decisions about the proceeds of the pool [24] to allowing peers to adjudicate their pool's claims.

From Wikipedia, the free encyclopedia. Retrieved 3 October Retrieved 5 September Archived from the original on 5 May Retrieved 24 January Retrieved 12 September Archived from the original on 1 October Retrieved 29 April Retrieved 20 December Retrieved 1 July Retrieved 22 September Retrieved 25 March Coverager -The Community of Insurance. Retrieved 6 October Retrieved from " https: Types of insurance Institutional investors Peer-to-peer introductions. CS1 French-language sources fr Use dmy dates from May All articles with unsourced statements Articles with unsourced statements from June Views Read Edit View history.

This page was last edited on 22 April , at By using this site, you agree to the Terms of Use and Privacy Policy.