Binarycom bot dashboard settingsresult

35 comments

Bitcoin mhash chart

Initially pioneered by financial institutions during the s as interest rates became increasingly volatile, asset and liability management often abbreviated ALM is the practice of managing risks that arise due to mismatches between the assets and liabilities.

The process is at the crossroads between risk management and strategic planning. It is not just about offering solutions to mitigate or hedge the risks arising from the interaction of assets and liabilities but is focused on a long-term perspective: Thus modern ALM includes the allocation and management of assets, equity, interest rate and credit risk management including risk overlays, and the calibration of firmwide tools within these risk frameworks for optimisation and management in the local regulatory and capital environment.

Often an ALM approach passively matches assets against liabilities fully hedged and leaves surplus to be actively managed. The exact roles and perimeter around ALM can vary significantly from one bank or other financial institutions to another depending on the business model adopted and can encompass a broad area of risks. The traditional ALM programs focus on interest rate risk and liquidity risk because they represent the most prominent risks affecting the organization balance-sheet as they require coordination between assets and liabilities.

But ALM also now seeks to broaden assignments such as foreign exchange risk and capital management. The ALM function scope covers both a prudential component management of all possible risks and rules and regulation and an optimization role management of funding costs, generating results on balance sheet position , within the limits of compliance implementation and monitoring with internal rules and regulatory set of rules.

ALM intervenes in these issues of current business activities but is also consulted to organic development and external acquisition to analyse and validate the funding terms options, conditions of the projects and any risks i.

Today, ALM techniques and processes have been extended and adopted by corporations other than financial institutions; e. For simplification treasury management can be covered and depicted from a corporate perspective looking at the management of liquidity, funding, and financial risk.

On the other hand, ALM is a discipline relevant to banks and financial institutions whose balance sheets present different challenges and who must meet regulatory standards.

For banking institutions, treasury and ALM are strictly interrelated with each other and collaborate in managing both liquidity, interest rate, and currency risk at solo and group level: Where ALM focuses more on risk analysis and medium- and long-term financing needs, treasury manages short-term funding mainly up to one year including intra-day liquidity management and cash clearing , crisis liquidity monitoring. The vast majority of banks operate a centralised ALM model which enables oversight of the consolidated balance-sheet with lower-level ALM units focusing on business units or legal entities.

It has the central purpose of attaining goals defined by the short- and long-term strategic plans:. Relevant ALM legislation deals mainly with the management of interest rate risk and liquidity risk:. Note that the ALM policy has not the objective to skip out the institution from elaborating a liquidity policy.

In any case, the ALM and liquidity policies need to be correlated as decision on lending, investment, liabilities, equity are all interrelated. The objective is to measure the direction and extent of asset-liability mismatch through the funding or maturity gap. This aspect of ALM stresses the importance of balancing maturities as well as cash-flows or interest rates for a particular set time horizon.

For the management of interest rate risk it may take the form of matching the maturities and interest rates of loans and investments with the maturities and interest rates of deposit, equity and external credit in order to maintain adequate profitability. In other words, it is the management of the spread between interest rate sensitive assets and interest rate sensitive liabilities..

Gap analysis suffers from only covering future gap direction of current existing exposures and exercise of options i. Dynamic gap analysis enlarges the perimeter for a specific asset by including 'what if' scenarios on making assumptions on new volumes, changes in the business activity, future path of interest rate, changes in pricing, shape of yield curve, new prepayments transactions, what its forecast gap positions will look like if entering into a hedge transaction This aspect of liquidity risk is named funding liquidity risk and arises because of liquidity mismatch of assets and liabilities unbalance in the maturity term creating liquidity gap.

Even if market liquidity risk is not covered into the conventional techniques of ALM market liquidity risk as the risk to not easily offset or eliminate a position at the prevailing market price because of inadequate market depth or market disruption , these 2 liquidity risk types are closely interconnected.

In fact, reasons for banking cash inflows are:. Measuring liquidity position via liquidity gap analysis is still one of the most common tool used and represents the foundation for scenario analysis and stress-testing. To do so, ALM team is projecting future funding needs by tracking through maturity and cash-flow mismatches gap risk exposure or matching schedule. In that situation, the risk depends not only on the maturity of asset-liabilities but also on the maturity of each intermediate cash-flow, including prepayments of loans or unforeseen usage of credit lines.

In dealing with the liquidity gap, the bank main concern is to deal with a surplus of long-term assets over short-term liabilities and thus continuously to finance the assets with the risk that required funds will not be available or into prohibitive level.

As these instruments do not have a contractual maturity, the bank needs to dispose of a clear understanding of their duration level within the banking books. This analysis for non-maturing liabilities such as non interest-bearing deposits savings accounts and deposits consists of assessing the account holders behavior to determine the turnover level of the accounts or decay rate of deposits speed at which the accounts 'decay', the retention rate is representing the inverse of a decay rate.

The crisis however has evidence fiercely that the withdrawal of client deposits is driven by two major factors level of sophistication of the counterparty: But daily completeness of data for an internationally operating bank should not represent the forefront of its procupation as the seek for daily consolidation is a lengthy process that may put away the vital concern of quick availability of liquidity figures.

So the main focus will be on material entities and business as well as off-balance sheet position commitments given,movements of collateral posted For the purposes of quantitative analysis, since no single indicator can define adequate liquidity, several financial ratios can assist in assessing the level of liquidity risk. Due to the large number of areas within the bank's business giving rise to liquidity risk, these ratios present the simpler measures covering the major institution concern.

In order to cover short-term to long-term liquidity risk they are divided into 3 categories:. Indication of how much available cash the bank has to meet share withdrawals or additional loan demand. Help to gauge the bank's liquidity in the short-term as how well current liabilities are covered by the cash-flow generated by the bank thus shows its ability to meet near future expenses without to sell assets.

Adjustement of the current ratio to eliminate no-cash equivalent assets inventory and indicate the size of the buffer of cash.

Measure of the bank's current position of how much long term earning assets more than one year are funded with non core funds net short term funds: The lower the ratio the better. Measurement of the extent to which assets are funded through stable deposit base.

Simplified indication on the extent to which a bank is funding liquid assets by stable liabilities. Indication that the bank can effectively meet the loan demand as well as other liquidity needs.

As an echo to the deficit of funds resulting from gaps between assets and liabilities the bank has also to address its funding requirement through an effective, robust and stable funding model. Today, banking institutions within industrialized countries are facing structural challenges and remain still vulnerable to new market shocks or setbacks:.

After , financial groups have further improved the diversification of funding sources as the crisis has proven that limited mix of funds may turn out to be risky if these sources run dry all of a sudden. The asset contribution to funding requirement depends on the bank ability to convert easily its assets to cash without loss. From customers and small businesses and seen as stable sources with poor sensitivity level to market interest rates and bank's financial conditions.

This plan needs to embrace all available funding sources and requires an integrated approach with the strategic business planning process. The objective is to provide realistic projection of funding future under various set of assumptions. Dependencies to endogenous bank specific events such as formulas, asset allocation, funding methods This reserve can also referred to liquidity buffer and represents as the first line of defense in a liquidity crisis before intervention of any measures of the contingency funding plan.

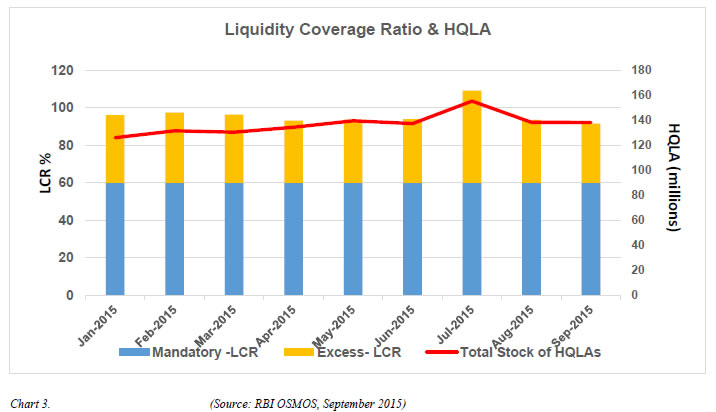

It consists of a stock of highly liquid assets without legal, regulatory constraints the assets need to be readily available and not pledged to payments or clearing houses, we call them cashlike assets.

As the bank should not assume that business will always continue as it is the current business process, the institution needs to explore emergency sources of funds and formalise a contingency plan. The purpose is to find alternative backup sources of funding to those that occur within the normal course of operations.

Dealing with Contingency Funding Plan CFP is to find adequate actions as regard to low-probability and high-impact events as opposed to high-probability and low-impact into the day-to-day management of funding sources and their usage within the bank.

These aspects can be expressed as the inability:. This assessment is realised in accordance with the bank current funding structure to establish a clear view on their impacts on the 'normal' funding plan and therefore evaluate the need for extra funding. This quantitative estimation of additional funding resources under stress events is declined for:.

In addition, analysis are conducted to evaluate the threat of those stress events on the bank earnings, capital level, business activities as well as the balance sheet composition. The last key aspect of an effective Contingency Funding Plan relates to the management of potential crisis with a dedicated team in charge to provide:. The objective is to settle an approach of the asset-liabilitiy profile of the bank in accordance with its funding requirement. In fact, how effectively balancing the funding sources and uses with regard to liquidity, interest rate management, funding diversification and the type of business-model the bank is conducting for example business based on a majority of short-term movements with high frequency changement of the asset profile or the type of activities of the respective business lines market making business is requiring more flexible liquidity profile than traditional bank activities.

Funding report summarises the total funding needs and sources with the objective to dispose of a global view where the forward funding requirement lies at the time of the snapshot.

The report breakdown is at business line level to a consolidatedone on the firm-wide level. This is the concept of Fund Transfer Pricing FTP a process within ALM context to ensure that business lines are funded with adequate tenors and that are charged and accountable in adequation to their current or future estimated situation.

From Wikipedia, the free encyclopedia. This article may need to be rewritten entirely to comply with Wikipedia's quality standards.

The discussion page may contain suggestions. Retrieved from " https: Banking Insurance Liability financial accounting Asset management. Wikipedia articles needing rewrite from May All articles needing rewrite. Views Read Edit View history.

In other projects Wikimedia Commons. This page was last edited on 28 April , at By using this site, you agree to the Terms of Use and Privacy Policy. Estimation of whether the business can pay debts due within one year out of the current assets: