Bitcoin stock plays

40 comments

Bitcoin projection chart

The opinions expressed in this article are those of the author and do not necessarily reflect the views of his employer or any other entity. It has garnered a lot of attention among technocrats and has also been written about extensively in the popular press. While its user base is still quite small compared to that of checks, credit and debit cards, and electronic funds transfers, a growing number of businesses are adopting bitcoin as a payment option for those customers who wish to use it.

Nationally known merchants such as Dell, Expedia, and Overstock. Even the United Way now accepts donations in bitcoin. This article examines the legal risks and issues that a business should evaluate before accepting bitcoin as a form of payment.

It provides a brief overview of bitcoin, addresses potential registration and licensing issues, and examines the tax implications of accepting the virtual currency. This article also discusses the use of bitcoin merchant service providers BMSPs , which act as intermediaries between a business and a customer wishing to pay in bitcoin.

The BMSPs provide a range of services including accepting bitcoin and paying the merchant in dollars, removing many of the barriers to accepting this new payment mechanism. Bitcoin is an Internet-based virtual currency which can be used to transfer value between parties.

A bitcoin has no physical presence and no central authority administers the currency. It is not backed by any government and is not legal tender in any jurisdiction. It is not issued by or redeemable at any financial institution. A bitcoin only has value because other participants in the ecosystem ascribe value to it.

This is how new units of the virtual currency come into existence. That software may be located on a personal computer or smartphone or hosted in the cloud by a service provider. While bitcoin is sometimes described as an anonymous currency, every transaction is recorded in the publicly accessible block chain and is associated with a public key. Tying a particular public key to an individual or company may be difficult, but it can be done.

Bitcoin users, and merchants in particular, should assume that their bitcoin transactions are public knowledge. To make a payment, a person uses his or her cryptographic credentials to sign a transaction transferring some amount of bitcoin to another person and submits it to the block chain.

The miners perform the mathematic calculations necessary to verify the transaction, and if it is deemed authentic, update the block chain to indicate the transfer of ownership. The whole process takes a couple of minutes maximum. Once written to the block chain, the transaction is not reversible.

The price of a bitcoin relative to the U. In the early days of the virtual currency, it was worth on a few cents. Volatility is likely to be an aspect of the bitcoin market for the foreseeable future and consequently should be a consideration for businesses which engage in transactions denominated in bitcoin.

At both the federal and state levels, there are requirements that entities engaged in certain financial service activities register or obtain a license if they wish to operate within the jurisdiction.

While the boundaries of these laws are not always as sharply delineated as business lawyers might like, it seems reasonably clear at this point in time that a business which merely accepts bitcoin as a payment mechanism on its own behalf has no obligation to register or obtain a license. As is discussed below, however, the law in this area is in a state of flux and merchants accepting bitcoin are advised to stay current with developments which may affect them.

Along with the duty to register, an MSB is obligated to develop an anti-money laundering plan, keep certain records, and report certain transactions and other suspicious activity to the government. The Financial Crimes Enforcement Network FinCEN , the agency which administers the BSA, has issued guidance explaining when a bitcoin business might be deemed to be engaging in money transmission and thus be obligated to register.

For BSA purposes, money transmission is defined as the acceptance of currency or other value that substitutes for currency from one person, and the transmission of that currency or substitute to another location or another person by any means. Currency is defined to mean the legal tender of the United States or another country. Under these definitions, bitcoin is not a currency, but it is something that can substitute for currency, and thus its acceptance and transfer to another person or location would constitute money transmission.

In its guidance, however, FinCEN makes clear that when a person obtains bitcoin and uses it to purchase goods or services, there is no acceptance from and no transfer to another person. Consequently, a person or business that uses bitcoin solely for its own purposes and not for the benefit of another is not an MSB. Furthermore, the business may hold on to that bitcoin, exchange it for dollars, or even use it to pay a vendor and not trigger the rule.

A merchant that is careful to limit its use of bitcoin to its own purposes and does not provide bitcoin services to others should have no obligations under the FinCEN rules. At the state level, many jurisdictions also require entities engaged in money transmission to obtain a license and to meet certain requirements for safety and soundness, as well as consumer protection.

A few states have opined on the application of their money transmitter laws to bitcoin related businesses. Kansas reached a similar conclusion under its statute. These regulators did acknowledge, however, that bitcoin related businesses such as wallet providers, currency exchanges, and ATM operators which receive government-issued currency for certain purposes might still be covered.

The agency indicated that it is working on new regulations to address when virtual currency users are engaged in money transmission and noted that changes to the underlying statute may be necessary in order to keep up with the market place. New York has taken a different approach, proposing a regulatory scheme just for virtual currencies.

The rule, however, would not cover merchants accepting bitcoin in consumer transactions. It seems reasonable at this stage to conclude that a merchant that accepts bitcoin or other virtual currencies for its own account in order to facilitate the sale of goods and services will not need to be licensed by or register with any governmental entity.

The merchant should be careful, however, not to provide bitcoin related services such as transfer or exchange to its customers. And finally, because this body of law will continue to grow and change, the prudent business will actively monitor regulatory developments in this area. When a business or individual conducts a transaction in a foreign currency, there are special rules which govern how gains or losses from the exchange of foreign currency are handled for tax purposes.

Many bitcoin users assumed that those rules would also apply to virtual currencies. Such hopes were dashed by IRS guidance issued in March which concludes that, for federal tax purposes, bitcoin and other virtual currencies should be treated as property and not foreign currency.

This interpretation by the IRS has enormous business implications for merchants accepting bitcoin and has been criticized by commentators. The IRS explains that for tax purposes virtual currency should be treated as property and that general tax principles which apply to property transactions will govern the tax treatment of bitcoin. When the asset is later exchanged, if the fair market value has increased, then the owner has a taxable gain.

Imagine a merchant that acquires bitcoin in multiple transactions over a month during which the price of bitcoin fluctuates. Its basis in each individual bitcoin may be different depending on the market price at the time of the transaction. When the merchant decides to cash out some of its bitcoin for dollars, it will need to decide not just how much bitcoin to sell but also which particular bitcoins to part with — because exchanging this bitcoin over that bitcoin will determine the amount of a reportable gain or loss.

Needless to say, the amount of record keeping necessary to track the basis in each bitcoin and compute gains and losses makes it impractical for many businesses to accept bitcoin. One work-around for this problem is for a merchant to exchange bitcoins for dollars immediately upon acceptance before the fair market value of the asset can change. Lucky for merchants, third-party service providers exist to offer just this type of service.

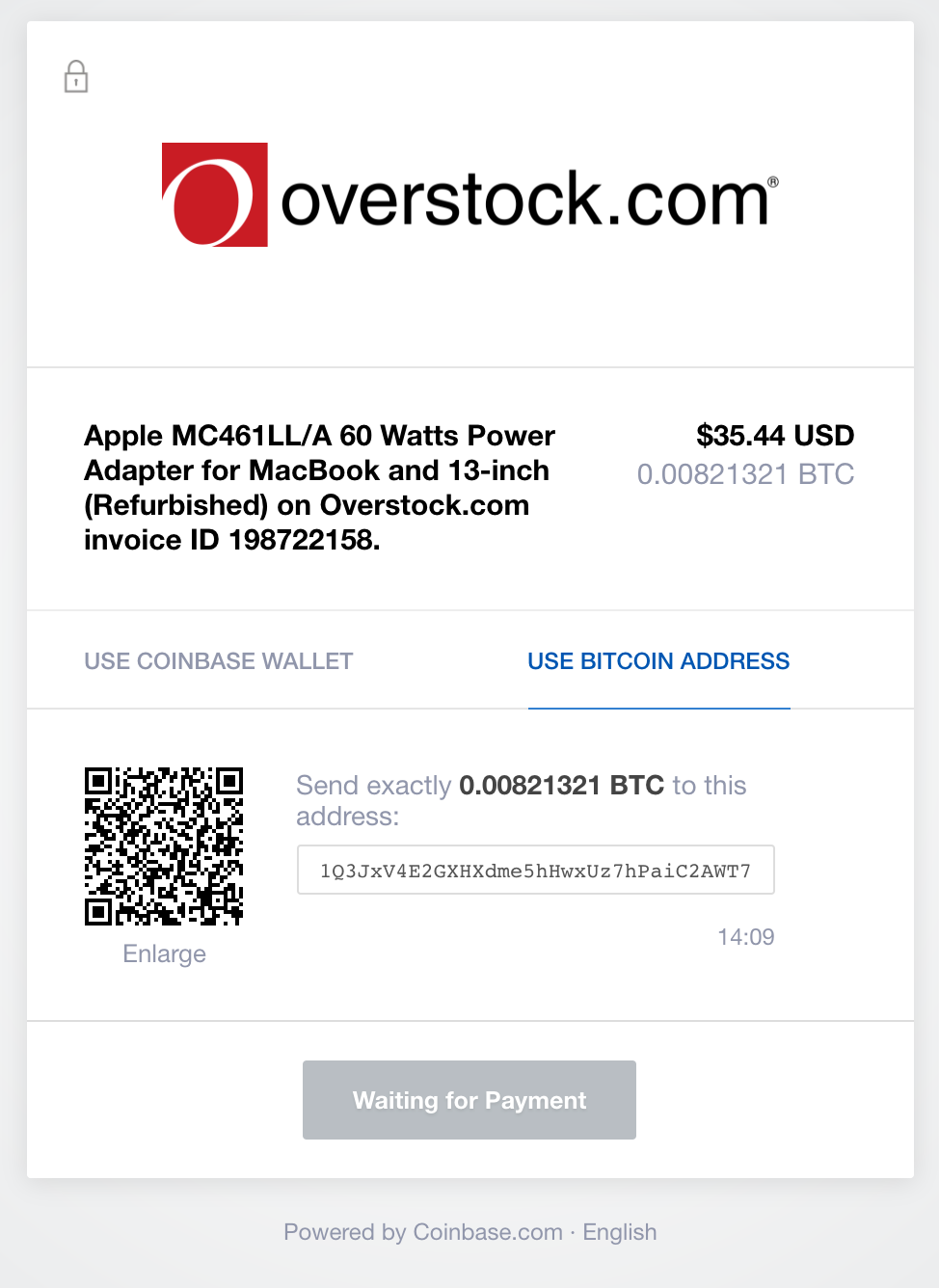

In response to the tax accounting and record-keeping issues described above and other legal and operational problems facing merchants which wish to accept bitcoin, a new category of service provider has emerged — the BMSP. Coinbase and BitPay are probably the best known of this class of vendors, but a quick Internet search reveals a growing number of players in this space.

The BMSP essentially acts as an intermediary, accepting bitcoin from the customer and providing dollars or some other currency to the merchant. The BMSP initiates the bitcoin transfer and notifies the merchant when the bitcoin transaction is complete. The merchant then completes the purchase transaction with the customer and ships the goods. The BMSP settles with the merchant on a prearranged schedule, usually daily, by electronically transferring dollars or euros or some other supported currency to a bank account designated by the merchant.

Some BMSPs also support settling in bitcoin or other virtual currencies. While pricing varies, several providers offer plans with no transaction fees. An obvious benefit of using a BMSP is that a merchant can enable its customers to pay with bitcoin without ever actually having to receive or hold bitcoin itself.

Such an arrangement would reduce or eliminate the accounting and record-keeping obligations associated with the IRS guidance, making virtual currency acceptance a significantly easier and more attractive option. Introducing an intermediary into the relationship with a customer, however, brings new risks which require careful evaluation. Before engaging a BMSP, a merchant might want to ask the following questions:. Given the increasing interest in bitcoin among the public, merchants understandably want to be able to accept it as a form of payment.

Managing the legal and tax implications associated with virtual currencies is a new challenge which business lawyers must address. The use of a properly managed BMSP can simplify the operational issues and reduce the legal risks of accepting bitcoin. The September issue of Business Law Today will feature topics and advice for business lawyers such as smart contracts, what structured negotiation can offer business attorneys, shareholder activism, and more.

Do you have a great idea for a BLT article? Would you like to see more of a featured column? Let us know how we can make Business Law Today the best resource for you and your clients. We welcome any suggestions. Please send us your feedback here. Business Bankruptcy August Consumer Financial Services June Corporate Governance July Cyberspace Law August Legal Opinions Spring Nonprofit Organizations Second Quarter, BLT is a web-based publication drawing upon the best of the Section's resources, including featured articles and other information from around the Section.

Stay informed on the latest business law practice news and information that will benefit you and your clients. Middlebrook About the Authors: Before engaging a BMSP, a merchant might want to ask the following questions: A BMSP accepts bitcoin from a consumer and provides dollars to the merchant. This action clearly constitutes money transmission under the BSA as discussed above. Ask the provider for a copy of its written anti-money laundering compliance program.

Is the BMSP a licensed money transmitter in the appropriate states? While there is more variance and uncertainty in state law, it seems likely that a BMSP would also be deemed to be a money transmitter in at least some states. A prudent merchant will determine if the BSMP is licensed in the jurisdiction in which the merchant operates, and if not, why not.

What is the settlement risk in using a BMSP and how can it be mitigated? Merchants should evaluate and understand this risk before engaging a BMSP.